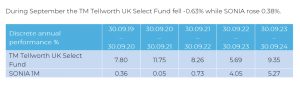

If August was characterised by working through the fall out from the Japan carry trade unwind, September was characterised by China and it’s surprise policy intervention to stimulate a weak economy and stabilise weak consumer confidence. The policy measures led to an unprecedented 30% increase in the Hang Seng Index and investors scrambled to cover China related underweights and reappraise portfolios in light of what the policy might mean for the China economy. Whilst the fund has insignificant exposure to China directly, the events led to significant rotation within the equity markets. Closer to home, the UK backdrop is almost entirely dominated by the Labour budget at the end of October, with very conflicting and vague tax proposals driving significant uncertainty at the index and company level; the FTSE250 Index underperformed the FTSE100 Index by 1.5% over the month to show this point.